One of the things that is hard for any investor to watch is increased market volatility and severe dips in the overall value of their portfolio. I'm no different than anybody else when watching the market tank and worrying about the value of my holdings. Currently the market is experiencing a decline due to a number of factors. China is devaluing the Yuan causing worry about the growth rate in the second largest market and potentially triggering a currency war. The FED is talking about raising rates, with some believing that it will now more likely happen in December instead of September due to the market conditions. Margin debt is at all time highs which typically occurs prior to crashes as people over leverage themselves to buy stocks that they feel can only go up. The United States is sitting on a debt bubble, not just the nation themselves, but also through student loans and retirement savings issues. I could go on and on, but I think I've created a fairly bleak picture based on the headlines of the moment.

What does this all mean to me as an investor? Nothing, in fact I'm rather excited about the prospects of a market correction. We're already down from highs in the 18,000 to close to testing 16,500 on the DOW and for those of us 30 somethings that have long term prospects I couldn't be happier. This market has been running on kool aid that the FED has provided along with central banks the world over and I think it's finally time that they are out of bullets to prop up this market. It's been a fun ride, but it's time that it corrects itself. People have lost fear and have been past the point of irrational exuberance for a while now. So what's my plan now that the market volatility has returned? Well first and foremost I do not plan to sell any stocks that are my core DGI holdings, this seems like a no brainer for us DGI folks, but it has been shown time and time again that people lose their ability to think long term when they are faced with the pain of a declining asset and market.

What I do plan to do is prepare my elephant gun to take on as many new stock opportunities as I can in the coming months or years. This alludes to what I mentioned in a prior post about if I knew what I know now in 2009, my portfolio would have been much larger and throwing off a lot more dividends. So what I plan on doing is throwing the savings into overdrive with minimal stock purchases in the near term. I smell a bargain coming as people start to become less confident in this market and when they start to flee with the blood in the streets is when I plan on starting to pounce. We've shed almost 1700 points from the all time high of 18,351.36 and I don't know if there's anything that the FED or other central banks can do to stop the bleeding, and I'm OK with that. Even though I've bled off almost $20,000 in my portfolio, mostly due to oil stocks, I'm ok with the fact that my dividends will go farther now in purchasing more shares to throw off an ever increasing passive income stream. I'm sure we'll probably see some positive days in the coming weeks and maybe even a nice bounce up for a bit, but I have a feeling more pain than pleasure is coming and I'm preparing for the opportunities ahead. This doesn't mean I'm not currently investing as I still have my 401k investing biweekly, but it does mean that I'm holding off on my personal picks as I see how things play out. I'm not trying to time the market, but rather getting more cautious as things take form.

What about you, are you changing your strategies with the increased volatility?

Another month and another time to look in at my smallest passive income stream, but one that I look at as my play money. Probably not the best way, but I've invested $50 a month to invest in a couple new micro loans each month (on top of the interest payments) and I like what I'm seeing so far. I've had a pretty good run the last month with my seasoned loans increasing, those loans that are over 10 months, and the return on investment starting to creep back up again. So here's a breakdown since last month.

As you can see compared to last month I've had some nice trending. I haven't invested the money this month basically because I forgot to and I don't like the auto invest feature as I have certain metrics that I look at and won't touch loans if they don't meet that criteria. I'm also not a fan of a robot selecting my loans for me.

So looking from last month to this month my rate of return has increased by almost 3% which is amazing for a one month comparison. My seasoned loans scored even better going from 5.17% to 8.38% which is an even more amazing 3.21% increase over last month. To put the rate of return in context here's a breakdown since I have started in January of 2014.

Clearly I'm doing pretty well despite a couple of deadbeats which were charged off. Overall the trend is very healthy and I'm quite pleased with the returns. Has anyone tried Prosper since my last post? If so please share your results and experiences.

Ah another month and now my second post on my passive income stream. I like to think of this as my freedom from doing what others want me to do as I'm really liking the current volatility that I'm seeing right now. My portfolio is down, but I'm building some cash reserves for what I see as the taper tantrum that is coming when the fed finally raises rates. I think the market has some of it prices in, but I'm almost certain tat people will freak and give us a buying opportunity on some REITs and other assets that will help propel my portfolio forward. That being said let's look at a breakdown of my July income:

Roth

IRA

Investment

Total

January

39.87

121.93

172.97

334.77

February

265.53

105.44

110.36

481.33

March

205.87

430.79

82.56

719.22

April

41.46

124.5

159.04

325

May

287.29

118.82

95.75

501.86

June

270.12

341.4

50.83

662.35

July

88.97

217.61

160.17

466.75

August

0

September

0

October

0

November

0

December

0

1199.11

1460.49

831.68

3491.28

In July my passive income was $466.75 versus my 2014 income of $339.81. This is an increase of 37.356169624201755% (love the oddly specific percentages) which is fantastic. This is another huge increase over 2014 and one more step closer to financial independence. As you can see though the bulk of my dividends are in my IRA so long term wise I have a lot of work to follow up on my investment account to allow me to retire early. Overall I'd say I had a pretty solid month and my investment account is starting to pull its own weight as it is coming to be more and more in line with my other accounts which are my heavier hitters. I'm hoping to see the current volatility continue and begin to top off this account to really start to propel my returns.

How did you all do in July, share your journey to fiscal freedom!

I don't usually use social media. Ironic since I'm a blogger these days, but I don't ever post on facebook, I never really used myspace, I'm instagram illiterate, and overall I really don't understand the gravitation to these sites. I can conceptually understand that it is nice to know what people are doing with their lives and stay in touch, but I thought that's what a phone and now text is for. However, being that it's the preferred medium for communication with a number of my friends, I've pretty much resigned myself to knowing that I need to at least have an account and check it on occasion. This brings me to really needing to rant about what Facebook has become.

In the beginning Facebook was cool, hip, and trendy. It was a closed community where only certain schools had access to it. I remember being in college and hearing about this cool new system to keep in touch and know what friends were up to. This was back in the days of AOL IM and it sounded like a really cool idea. Fast forward a bit and it was made available to everyone. I joined, played around a bit, and found that it was kind of neat to see where my friends were and what they were doing. Then EVERYONE joined and things started to spiral out of control.

Don't get me wrong I think Facebook is a cool way to stay in contact and when I first got on that's what everyone did. Then the start of menial tasks came about. Status updates like "I'm in bed" or "I'm in the bathroom" started to pop up. What originally was a fun way to see what people were up to turned quickly into a toilet bowl of complete and utter crap. I'm sorry but if you're dropping the kids off in the pool I DON'T want to know. EVER! We all use the bathroom, we just don't need to glorify and commemorate it for the world to see.

Next came the influx of pictures of what people were going to eat. Hit a restaurant, take a picture of the well cooked meal and post it on Facebook. My reaction every time I saw these posts...Neat you eat food. Why do I care what food you are eating. How does this connect me to you as a person? This type of stuff drove me crazy and was part of the reason I started to use the site less and less. Facebook was slowly transforming into a commemoration of blandness. We didn't talk about the amazing experience we had in Costa Rica as much as the salad we had at Denny's.

Fast forward to now and my utter disgust and frustration with social media in general. There are things you just don't talk about with other people on a global scale. Things like money, religion, or politics are taboo for a reason. Facebook has become the mother of all dumping grounds for our political and religious views and we lurch from one politically correct crisis to another with people chiming in on both sides of the viewpoints. What happened to the days where we were not guilty until proven innocent? When we didn't castrate a person for a particular viewpoint, but rather worked out our differences and came to a mutually acceptable plan of action? This gets into politics which I don't want to touch on, but Facebook has become the mainstream way of expressing out views into these subjects. I respect everyone's opinions on subjects. Your for gay marriage? Great! You think that being atheist is the best for people? Good for you! You want to marry your toaster? Fantastic!

The point is we're forcing viewpoints and political arguments on our friends, many who have opposing viewpoints, and then we shame each other for the world to see. Facebook was supposed to be about connecting each other positively and it seems like we're moving away from that and into more of a world where we are dividing ourselves even more. I have friends who don't have spirited debates, but rather falling outs because of their Facebook activities. I long for the day when Facebook and all social media was about connecting to those around the world in its purest form and not a representation of all the opinions of people that spark insanity.

What about you, how do you feel about Facebook and is it an integral part of your life?

As we all know in 2008 the market tanked. The sky was falling, federal bailouts were the norm, and people were seeing blood in the streets. Lehman brothers failed and went into bankruptcy, Bank of America bought Countrywide (a poor decision) and Merrill Lynch (an even worse one, and in the following years a ton of bank failed. While some can argue that the government forced some of the purchases, Bank of America's for example, this period in American financial history proved to be one of the greatest economic opportunities for us investors if we had had the stomach and the guts to invest during this time period. If I knew then about dividend growth investing what I know now about it, well life would be very different indeed.

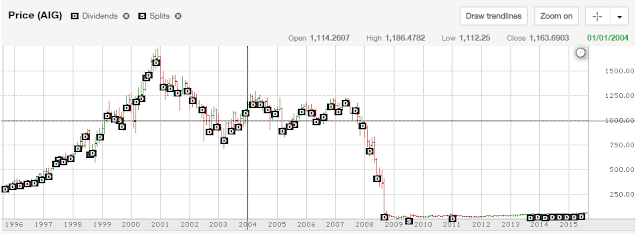

So fast forward to post recession economics where once great companies have sullied reputations, auto makers are booming again, and interest rates are still non-existent. Dividend income is where it's at and the once great dividend powerhouses that helped millions work towards financial freedom were crushed. There are times during investing that you have to take a chance and make some smart, educated gambles. So on March 13, 2014 I took a close look at American International Group (AIG) and liked what I saw. To understand why this was a gamble one need only to look at the recent history of this once enviable organization.

American International Group is one of the largest insurers in the world and when the financial crisis hit it was one of the first "too big to fail moves" The federal reserve stepped in and bailed out AIG to the tune of $85 billion and this is when AIG suspended their dividends. To get a better understanding here is a quick breakdown of the events around AIG circling into it's demise:

A – 9/15/2008 Collapse of Lehman Brothers: This is widely regarded as the event that set the financial crisis in motion.

B – 9/19/2008 AIG Pays a Dividend: This would be the last dividend AIG would pay for five years.

C – 9/23/2008 AIG Officially Suspends Dividend: The government bailout forced the company to suspend its dividend.

D – 8/1/2013 AIG Officially Reinstates Dividend: After strong earnings, the company announced that it would bring back its dividend distribution.

E – 9/26/2013 AIG Pays a Dividend: In its first dividend in 5 years, AIG paid out $0.10 per share to its shareholders.

To really understand how much this company fell off a cliff let's look at what the value of the stock was and paying a hefty $4.40 dividend!

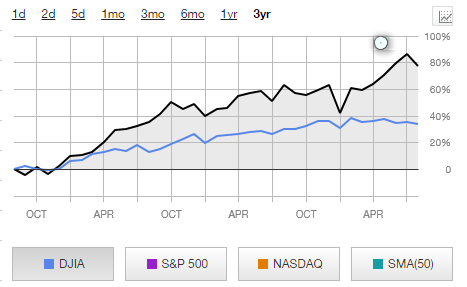

This chart is really telling, AIG was CRUSHED during the financial crisis and prior to it it was a high flying company. So how has AIG looked the last three years?

As you can see it has handily outperformed the DOW and is up almost 80% in that time period. Since I have bought the dividend has been at $0.125 per share, a far cry from that $4.40 mark only a few short years ago. Yesterday AIG made a huge dividend announcement coupled with a new $5 billion share buyback program.

The big news for me is that the dividend increased a whopping 124%, that's a huge increase and a big vote of confidence for the company's future in my opinion. This increase adds $125.39 a year in dividend income. This is fantastic and proof that ever once in a while taking a calculated risk is worth the chance.

Tell me about your best calculated risk and why you did it.

The online financial community has a plethora of options available to them to manage their financial lives online. I'd like to talk about two of the better options out that, the benefits, and the detractors of each. These services are Mint and Personal Capital, both linked for convenience and not to generate a referral bonus. Each of the companies do some things extraordinarily well in their current iterations, but of course each has room for improvement as well. So which is better?

Personal Capital

Personal Capital is a fantastic free online tool that allows you to see your overall net worth, manage your accounts, and see trends over time. I personally like this tool to track net worth as it provides easy to read graphs and trending over the month to see where your money has gone. To top it off it allows you to see how you are allocated by sector and determine if you are overweight or underweight a particular asset class. To me it's a really cool tool to see where everything is without having to create all of my own custom tools to do so.

Another cool tool is the ability of Personal Capital to recognize my pension versus my 401k. Yes I'm one of the few that still has both and I'm extremely lucky to be in this camp. Personal Capital is able to pull this data in, while Mint is unable to do so.

So what's the downside? On occasion Personal Capital will lost track of your accounts, which causes fluctuations in the graphs. I'm not really sure why this occurs, but on a fairly consistent basis it loses touch with my Ameritrade account and my net worth falls a hundred thousand dollars. This makes it difficult to see the true trending of my accounts as having my net worth crater once a month skews the actual results. In addition to this Personal Capital does not really update as quickly as its peer and credit transactions take longer to update.

Mint

Mint is another fantastic free online tool to help you manage your money, It really is a simple interface and anyone who was familiar with Quicken will recognize many of the same features. Mint was ultimately purchased by Intuit and supplements the Quicken experience. I like Mint for a variety of reasons. First it updates faster than Personal Capital. It recognizes pending transactions and reports on them ASAP. This is really nice for when I get paid and when I purchase any items as bank accounts reflect things a day earlier than Personal Capital will. In fact Mint recognizes pending transactions on my credit card within five minutes of the actual purchase. This really provides a truer perspective on where my money is at all times. FANTASTIC!

The downside to Mint? Well first it doesn't recognize my pension. In fact it can't even find it even though it's located on the same site as my 401k. Somewhat surprising and disappointing, but I make due. Second, the graphs are not as robust or as helpful as Personal Capital. In fact, in my opinion, the long term trending of Mint is pretty abysmal. I like it for it's short term and the ability to see where my money has gone recently.

So Who Wins?

In the case of Personal Capital versus Mint I can clearly state that the winner is......

Neither. Both have their perks and detriments, but neither is really superior to the other. In fact I would argue that to truly understand your current fiscal state the use of both is necessary. I like facets of both products and encourage those seeking financial freedom to use them. But understand that there are some limitations to them and knowing that they are tools to help watch your overall goals.

So what are your thought? Which tools do you use to manage your financial life?

As I like to have a diversified stream of revenue I try to look at all of my different options in generating a return on investment. One of the avenues I dabble in is prosper.com, this site allows me to become a creditor for small consumers or businesses that aren't getting loans in the traditional sense. Peer to peer lending is a relatively new wealth building tool and one that carries its own set of risks. What if the market gets weak again, will the borrowers be able to pay? What about people who are out there to game the system? Will the big boys get involved and scoop up all of the lucrative loans?

All of these are viable questions and the reason why I try to keep my exposure to peer to peer loans somewhat small as an overall risk. My account is also only a year old so it is relatively small. Whether I decide to grow it faster will be determined by the annual returns over a couple of years as I get my feet wet in these uncharted waters. So how does Prosper rate their loans for those of us willing to invest. Below is a table with the results into 2014. Not completely up to date, but stille relevant for my purposes..

As you can see there are seven different loan qualities with average yields from 7% all the way up to almost 27%. While this was relevant in 2014, I tend to find that the AA loans are a little lower right now on their yields. AA loans are obviously the highest quality, while HR loans are extremely risky. Although I see it on their table, I have yet to see an HR loan make it to the marketplace. This is probably due to some of the larger players buying them before the general public. At this point I've dabbled between AA and E loans and while most loans have paid their principle and interest payments on time, I've found that I have issues with C rated loans the most. This has skewed me into a more conservative lending rate and focusing on the AA and A loans primarily, with the odd B-E loan making it in.

What's nice is that Prosper will also break down your returns based on if they are "seasoned", those loans that are ten months or older, and then the all in number. Loans on prosper tend to stay up to date once they make the ten month window. There is apparently a lot higher default rate before then. So what are my returns after dabbling with peer to peer lending for the last year? Below is my current breakdown and account size.

Small account size, but not bad considering I maxed out my roth, 401k, and added about six grand to my investment account last year. I like the fact that I get paid monthly on the loans and that I can. quickly reinvest the proceeds on a monthly basis. It's a lot like having a dividend stock that pays you ever month instead of quarter, it allows you to build up the capital to purchase more faster. I don't have any loan that is over $25.00 which allows me to spread the risk across a great variety of individuals. This helps to mitigate any risk that any one individual can cause to my portfolio. As of now, prosper claims that anyone with a portfolio over $2500.00 has not lost money in the marketplace. As my account grows, it will be interesting to see if this is the case or not.

How about you? Have you tried peer to peer? If so what experiences do you have with peer to peer lending?

As you can see compared to last month I've had some nice trending. I haven't invested the money this month basically because I forgot to and I don't like the auto invest feature as I have certain metrics that I look at and won't touch loans if they don't meet that criteria. I'm also not a fan of a robot selecting my loans for me.

As you can see compared to last month I've had some nice trending. I haven't invested the money this month basically because I forgot to and I don't like the auto invest feature as I have certain metrics that I look at and won't touch loans if they don't meet that criteria. I'm also not a fan of a robot selecting my loans for me.

As you can see there are seven different loan qualities with average yields from 7% all the way up to almost 27%. While this was relevant in 2014, I tend to find that the AA loans are a little lower right now on their yields. AA loans are obviously the highest quality, while HR loans are extremely risky. Although I see it on their table, I have yet to see an HR loan make it to the marketplace. This is probably due to some of the larger players buying them before the general public. At this point I've dabbled between AA and E loans and while most loans have paid their principle and interest payments on time, I've found that I have issues with C rated loans the most. This has skewed me into a more conservative lending rate and focusing on the AA and A loans primarily, with the odd B-E loan making it in.

As you can see there are seven different loan qualities with average yields from 7% all the way up to almost 27%. While this was relevant in 2014, I tend to find that the AA loans are a little lower right now on their yields. AA loans are obviously the highest quality, while HR loans are extremely risky. Although I see it on their table, I have yet to see an HR loan make it to the marketplace. This is probably due to some of the larger players buying them before the general public. At this point I've dabbled between AA and E loans and while most loans have paid their principle and interest payments on time, I've found that I have issues with C rated loans the most. This has skewed me into a more conservative lending rate and focusing on the AA and A loans primarily, with the odd B-E loan making it in.